Trending on Billboard

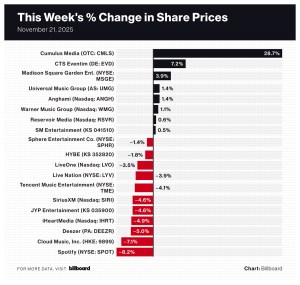

Spotify’s stock price has fallen more than $200 below its all-time high of $785.00 set on June 27 after falling 8.2% to $583.62 in the week ended Friday (Nov. 21). The Swedish streaming giant’s share price dropped more than 7% in the two days after it announced the purchase of WhoSampled, an online song samples database, to power a new song credits feature, SongDNA.

Investors’ reaction to a relatively small acquisition appears to be part of a larger theme in recent weeks. While Spotify is one of the better-performing music stocks of 2025, it has struggled since the company announced on Sept. 30 that CEO Daniel Ek will step down and assume the role of executive chairman. Ek attempted to assuage investors who might be wary of his departure, saying in an open letter that “very little will change” when Spotify is led by co-CEOs Alex Norström and Gustav Söderström, two longtime Spotify executives. Ek added that he will operate with a European-style approach to the executive chairman position that is “more hands-on than the traditional U.S. model.”

Related

![]()

But investors aren’t showing much faith in the post-Ek era. Since the announcement, Spotify shares have fallen 19.9%, erasing $29.7 billion of market value.

Driven by Spotify’s 8.2% decline — the worst for all music companies this week — the Billboard Global Music Index (BGMI) fell 4.8% to 2,571.67. Eight of the index’s companies had gains while 11 finished the week with losses. The BGMI has not posted a gain in 10 weeks and now stands 17.5% below the all-time high of 3,117.20 set during the week of June 30.

Markets were down around the world this week. In the U.S., the Nasdaq fell 2.7% to 22,273.08 and the S&P 500 dropped 1.9% to 6,602.99. The U.K.’s FTSE 100 sank 1.6% to 9,539.71. South Korea’s KOSPI composite index and China’s Shanghai Composite Index each dropped 3.9%.

Warner Music Group (WMG) finished the week up 1.1% to $30.69. After releasing earnings on Thursday morning (Nov. 20), WMG shares dropped 2.7% on Thursday but gained 3.4% gain on Friday. Investors may not have received their desired message from WMG management, but analysts were upbeat about the numbers and management’s outlook. CFRA bumped WMG shares up to a “hold” rating from the “sell” rating it issued in July. Guggenheim kept its “buy” rating and $37 price target while noting that WMG’s “capital efficient” joint venture with Bain is likely to provide growth to both revenue and earnings. J.P. Morgan, which maintained its “overweight” rating and $40 price target, was “encouraged” by WMG management’s comments on margin expansion and market share gain.

Related

CTS Eventim shares rose 7.2% to 84.65 euros ($97.52). The German concert promoter and ticketing company released third-quarter earnings on Thursday that showed revenue rose 4%. The week’s gain brought CTS Eventim’s year-to-date gain to 0.8%.

Netease Cloud Music fell 7.1% to 189.40 HKD ($24.33) after its third-quarter earnings, released on Thursday, revealed a 2% decline in revenue. Cloud Music remains one of the year’s best-performing music stocks, however, with a 2025 gain of 68.8%.

Live Nation shares fell 3.9% to $130.55. Deutsche Bank lowered its price target to $160 from $173, which suggests 22.6% of upside based on Friday’s closing price, and maintained its “buy” rating.

The week’s greatest gainer was Cumulus Media, which rose 29% to $0.11. Such large swings are common for Cumulus, which has lost 85.7% of its value in 2025 and experiences sizable moves when it rises or falls a mere penny. With a market capitalization of just $2 million, the radio broadcaster has little effect on the BGMI.

Billboard.com

Billboard.com

Billboard.com

What our fans have to say